We have entered what I am calling the “High-Friction Era.” For thirty years, the global trade narrative was a one-way street toward efficiency, cost-optimization, and “just-in-time” magic. But as we sit here in the first quarter of 2026, that era hasn’t just ended—it has been dismantled and replaced by a far more expensive, far more volatile, and far more political reality.

If you are a sourcing professional, a CEO, or a hedge fund manager looking at the next three months, you aren’t just managing a supply chain anymore. You are managing a geopolitical portfolio. The math of global trade is no longer just about the unit price in a Dongguan factory; it is about the risk premium of a missile in the Red Sea and the regulatory hurdles of a “fragmented” world order.

Here is the memo on the structural rewiring of the world economy for the next 90 days.

I. The View from Beijing: “Quality” Over “Velocity”

To understand the next quarter, you have to start with the signals coming out of the Great Hall of the People. The Chinese government has officially launched the 15th Five-Year Plan (2026-2030), and the message is one of strategic recalibration.

The Official Stance:

Premier Li Qiang, in his recent government work report, set the 2026 GDP growth target at a cautious 4.5% to 5%. This isn’t a sign of weakness; it’s a pivot toward “high-quality development”. Beijing is signaling a readiness to sacrifice raw speed for “new quality productive forces”—shorthand for AI, green energy, and self-reliant tech stacks.

The Analyst View:

Beijing is effectively “hunkering down.” They are bracing for a prolonged period of external turbulence while doubling down on internal resilience. For global buyers, this means your Chinese partners are likely to be more stable than their neighbors, but they will be operating under a “state of caution.” Expect tighter credit and a laser focus on high-tech exports like EVs and semiconductors.

II. The Middle East Shock: The “Hormuz-Suez” Factor

If China is the engine, the Middle East is the fuel line—and that line is currently under immense pressure. The ongoing Red Sea crisis has introduced a “Risk Premium 2.0” into every transaction.

The Assessment:

We are watching the most significant disruption to maritime logistics since the pandemic. With major carriers like Maersk and COSCO frequently rerouting around the Cape of Good Hope, the “time value of money” has changed.

The 90-Day Trading Effect:

- Logistics Surcharges: Expect ocean freight rates to climb another 15% to 25% through June. Carriers are already baking in the cost of 10–14 days of extra sailing time.

- Insurance Withdrawal: War-risk premiums are surging. If your goods aren’t properly covered, they simply don’t move.

- The “Hormuz Factor”: Any escalation toward the Strait of Hormuz would move us from a “logistics delay” to an “energy catastrophe”.

III. The Strategic Evaluator: The Death of “Free Trade”

My individual assessment is that we have entered the age of “Managed Trade.” The “Andrew Ross Sorkin” types in Davos once talked about a borderless world; today, we have three distinct trading blocs:

- The China-Global South Axis: Beijing is deepening ties with the Middle East (ASEAN and Arab states), moving toward “institutional opening up” that bypasses Western sanctions.

- The U.S. Protectionist Shield: “Trump 2.0” rhetoric and universal baseline tariffs have forced a permanent redirection of flows toward Mexico and Vietnam.

- The EU Regulatory Wall: Europe is becoming the world’s “Chief Compliance Officer,” using carbon taxes (CBAM) to gatekeep trade.

The Effect: You no longer have one supply chain. You have three, and they are increasingly incompatible. If you are sourcing for the U.S. market from China, your “De-Minimis” exemptions are likely on the chopping block.

IV. Three-Month Outlook: April – June 2026

If I am sitting in your seat, here is the playbook for the next 90 days:

1. The Post-NPC Surge (April)

Following the National People’s Congress, expect a wave of industrial subsidies aimed at “AI+” technologies. This will create a temporary surge in component supply, but it will likely trigger “retaliatory tariffs” from the West.

- The Move: Front-load your high-tech orders in April before the next round of trade friction begins.

2. The Inflationary Ripple (May)

The energy spikes from the Middle East will hit the factory floor in May. Chinese manufacturers are already seeing their input costs rise.

- The Analyst View: We are moving from “Goods Deflation” to “Input Inflation.” For the first time in years, Chinese factories will have the leverage to raise prices because the alternative—sourcing from a less stable region—is even riskier.

3. The RMB Paradox (June)

The PBOC (People’s Bank of China) maintains a “prudent” monetary policy. However, as the U.S. Dollar stays strong as a “safe-haven” during regional conflicts, the RMB will face natural downward pressure.

- The Strategy: Use the current window to lock in currency hedges. The volatility in June could be the highest we’ve seen this decade.

V. Supporting Evidence: Global Responses

- Beijing: Foreign Minister Wang Yi has articulated the “Four Respects” framework, signaling that China will prioritize partners who respect its “core interests” and “sovereignty”.

- Washington: The U.S. Treasury continues to tighten sanctions on Iranian oil entities, indirectly impacting the “dark fleet” that supplies China, which could lead to sudden energy spikes for manufacturers.

- The IMF/World Bank: Both have revised growth forecasts, noting that while China is resilient, it is “too big” to rely solely on exports in a world that is increasingly building “Trade Walls”.

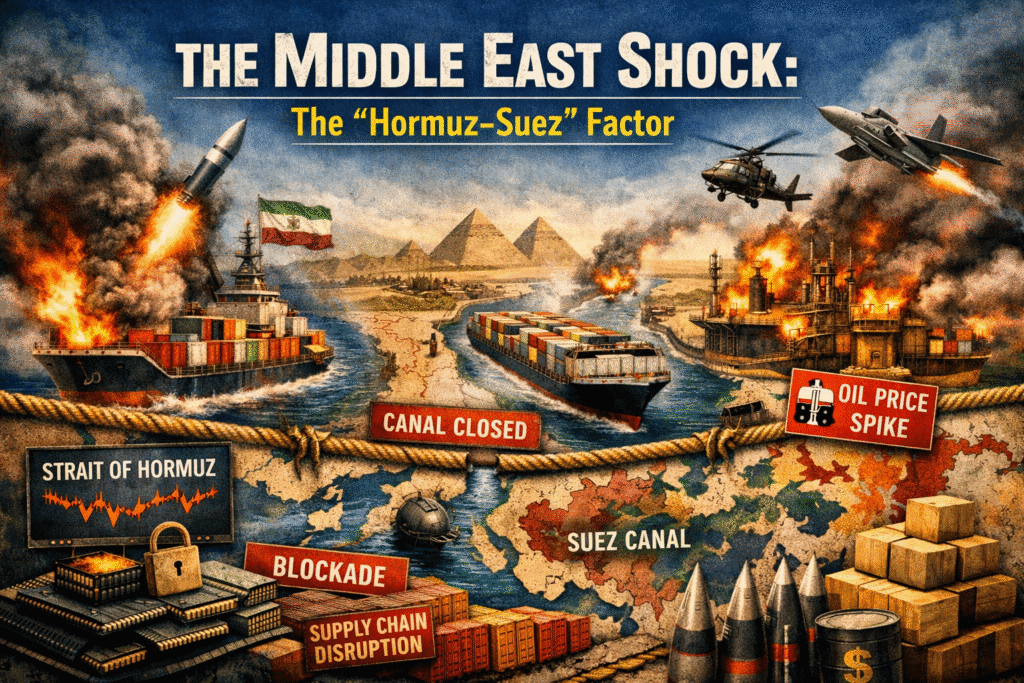

Financial Snapshot: Market Volatility (March 2026)

The divergence between the Hang Seng Index’s resilience and the extreme volatility in Global Shipping Bonds tells the real story: the “factories” are ready, but the “delivery trucks” are under fire.

The Bottom Line: The next three months will reward the agile and the liquid. In 2026, reliability is no longer a metric—it is the only currency that matters. If you haven’t secured your Q3 capacity by the time you finish this article, you are already late to the game.

References & Sources: