As global health systems face a $25 billion annual deficit due to logistics waste, procurement strategies are hitting a hard pivot. This comprehensive briefing analyzes the 5 critical shortages redefining the global medical device supply chain in 2026—from raw component scarcities and stereotactic biopsy needle deficits to strict material bottlenecks driven by the newly active FDA Quality Management System Regulation (QMSR). Discover how tier-one sourcing managers are discarding the fragile “Just-in-Time” model to build compliant, redundant vendor networks.

The Post-Pandemic Procurement Illusion and the Regulatory Catalyst

The global medical device market is operating under a false sense of stabilization, where traditional procurement methodologies no longer guarantee pipeline security. For years, business-to-business buyers relied on predictable lead times and linear fulfillment models, but a convergence of intense regulatory shifts, geographical choke points, and materials scarcity has permanently disrupted the standard baseline. The single greatest catalyst of this transformation is the official enforcement of the newly active Food and Drug Administration Quality Management System Regulation, which went into effect on February 2, 2026. This landmark rule replaces decades-old quality frameworks by incorporating international ISO 13485 standards directly into United States federal oversight.

For sourcing professionals and hospital procurement executives, this regulatory convergence means that purchasing controls are no longer just administrative checklists, but are now the primary focus of aggressive, risk-based federal inspections. Suppliers who fail to align with the new data-integrity mandates are being rapidly disqualified, causing immediate downstream availability issues. At the same time, logistics networks are straining under escalating Scope 3 carbon penalties and maritime security threats, forcing B2B buyers to abandon vulnerable single-source dependency. To navigate this highly complex landscape, sourcing guides across the industry are urging managers to dissect the specific item categories facing severe supply contractions. Five distinct product and material shortages are currently reshaping the medical procurement landscape, requiring strategic shifts in vendor diversification and inventory management.

1. Stereotactic Breast Biopsy Needles and Precision Diagnostic Tooling

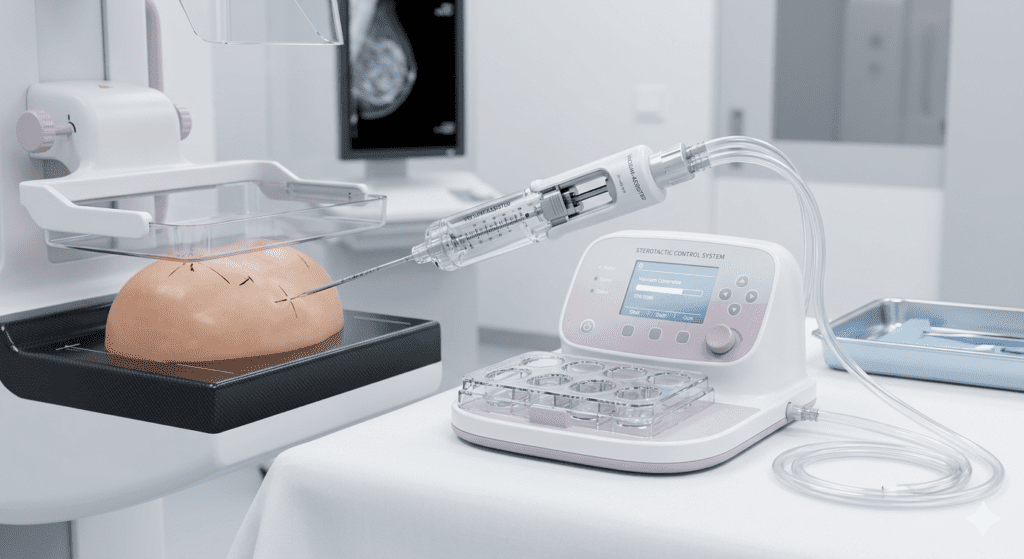

The diagnostic hardware sector is experiencing an unprecedented supply squeeze, particularly within specialized oncology components. The FDA Medical Device Shortages List formally tracks stereotactic breast biopsy needles under product code KNW due to severe market disruptions stemming from widespread manufacturing recalls and quality-control shutdowns. Because these high-precision instruments require incredibly exact tolerances and specialized cleanroom environments, buyers cannot easily substitute them with alternative product codes without delaying critical clinical procedures.

The shortage highlights a systemic vulnerability in the medical manufacturing sector, where a vast majority of regional health systems depend on a very small, concentrated group of tier-one suppliers. When a primary manufacturer faces a contamination issue or an unexpected factory closure, the entire clinical pipeline stalls almost instantly. To mitigate this specific vulnerability, B2B procurement managers are shifting away from rigid, multi-year exclusive agreements and are actively seeking secondary and tertiary manufacturing partnerships in alternative geographic zones.

2. Neurosurgical Patties, Sponges, and Specialized Consumables

The operational stability of surgical suites nationwide is facing major headwinds due to ongoing supply deficits in fundamental operating room consumables. Federal health agencies have issued formal alerts highlighting severe manufacturing disruptions for neurosurgical patties, sponges, and strip devices, with supply constraints expected to persist through the remainder of 2026. This shortage was triggered by out-of-specification endotoxin levels detected during routine manufacturing audits, which forced immediate recalls and localized factory halts.

While a surgical sponge may seem like a low-tech commodity compared to advanced robotic imaging systems, its absence completely halts high-margin neurosurgical and microsurgical workflows. B2B buyers have traditionally overlooked these lower-tier items, assuming that wholesale distribution networks possessed infinite buffer stock. This crisis has demonstrated that even basic consumables are highly vulnerable to localized quality failures, prompting procurement networks to mandate deeper visibility into the raw material origins of their distributors.

3. Micro-Electronics and “Golden Screw” Smart Components

The rapid proliferation of the Internet of Medical Things has created a massive, structural dependence on advanced electronic architecture, placing medical buyers in direct competition with consumer technology sectors. Modern connected hardware—ranging from ambulatory infusion pumps to wearable cardiac monitors—relies on specific micro-controllers, wireless transmitters, and sensors that are frequently subject to severe raw material allocations. In electronic sourcing, these essential parts are often referred to as “golden screws” because the absence of a single, inexpensive microchip entirely stalls the final assembly of a million-dollar diagnostic system.

The implementation of the updated FDA inspection models under the new quality regulations places intense pressure on electronics manufacturing services to verify the pedigree of every single micro-component. This elevated compliance baseline has extended lead times for sub-assemblies to unprecedented lengths, transforming what used to be a standard six-week fulfillment cycle into an uncertain multi-month timeline. Procurement executives are responding by forging direct relationships with component foundries rather than relying solely on third-party distributors, securing long-term allocations well in advance of final assembly needs.

4. Fluoropolymer Liners and PFAS-Compliant Raw Materials

A silent but incredibly disruptive material shortage is unfolding at the foundational chemistry level of medical device manufacturing. Global regulatory crackdowns on per- and polyfluoroalkyl substances, commonly known as forever chemicals, have sent shockwaves through the raw material pipelines that supply catheter liners, specialized guide-wires, and sterile barrier packaging. Because these materials possess unique, ultra-smooth and chemically inert properties, finding direct, high-performance substitutes that meet stringent biocompatibility requirements is proving to be exceptionally difficult.

As chemical manufacturers scale down their production of traditional fluoropolymers to comply with emerging environmental mandates, medical device builders are scrambling to secure the remaining certified allocations. B2B buyers are discovering that their traditional original equipment manufacturers are running low on the specialized inputs required to deliver finished diagnostic and interventional kits. Forward-looking procurement teams are actively auditing their entire supply architecture to identify which vendors are lagging in the transition to next-generation, compliant materials, ensuring they do not get caught in sudden regulatory production halts.

5. Sterile Barrier Packaging Materials and Tyvek Out allocations

The final and most pervasive bottleneck in the current medical device ecosystem centers on the validated packaging materials required to maintain product sterility from the factory floor to the sterile field. High-density polyethylene materials, which form the protective barrier for billions of single-use surgical instruments, are facing localized allocation constraints driven by shifting global production capacities and rising raw substrate costs. Without a fully validated, undamaged sterile barrier, even a perfectly manufactured implantable device is legally classified as non-concomitant and cannot be used in a clinical setting.

This packaging crunch is further complicated by new international sustainability laws that penalize excessive material waste and require higher proportions of circular, recyclable substrates. Balancing the absolute requirement for sterile preservation with aggressive corporate and regulatory environmental mandates has created a major sourcing bottleneck. Procurement organizations are responding by qualifying alternative packaging designs and diversifying their supply lines across regional converters, ensuring that finished goods do not sit immobilized in warehouses simply because they lack an approved external wrap.

Discarding Just-in-Time for Compliant Redundancy

The overarching lesson of the 2026 procurement landscape is that the historically praised Just-in-Time inventory model is structurally incompatible with modern healthcare security and strict regulatory oversight. When supply chains operate with zero margin for error, any minor disruption—whether a regulatory compliance audit, a material shortage, or a maritime delay—triggers a catastrophic cascade of product stockouts and financial losses. Tier-one procurement executives are actively dismantling these fragile structures in favor of a resilient, Just-in-Case architecture characterized by deliberate, regionalized buffer stocks.

Building this necessary redundancy requires a sophisticated, data-driven approach where buyers prioritize total supply chain visibility and strict vendor compliance over simple per-unit cost savings. By leveraging modern digital tracking networks, diversifying vendor portfolios across multiple geographic regions, and actively monitoring real-time federal shortage databases, B2B buyers can successfully insulate their organizations from sudden market contractions. Ultimately, securing the medical supply pipeline is no longer just a functional back-office obligation, but has become a vital strategic pillar that directly protects both operational margins and patient safety.